All the requirements and conditions to be fulfilled in case of related party transactions have been altered to be in line with the provisions of Companies Act, 2013.

“This is the provisions of SEBI (LODR), which are applicable with immediate effect from 2nd September, 2015; Passing of ordinary resolution instead of special resolution in case of all material related party transactions subject to related parties abstaining from voting on such resolutions.“

A. “RELATED PARTY” means a related party as defined under sub-section (76) of section 2 of the [1]Companies Act, 2013 or under the applicable accounting standards:

Not Applicable: This definition shall not be applicable for the Units Issued by Mutual Funds which are listed on a recognized stock exchange(s);

B. “RELATED PARTY [2]TRANSACTION” means

Condition-1

- A transfer of Resources,

- A transfer of Services or

- A transfer of obligations

Condition-2: Between a Listed Entity and a Related Party.

Condition-3: Regardless of whether a price is charged and

Non Applicability: This definition shall not be applicable for the units issued by mutual funds which are listed on a recognised stock exchange(s);

These provisions shall be applicable to all prospective transactions.

Regulation (24)

I. POLICY OF MATERIALITY: Listed entities shall formulate a policy on

Materiality of Related Party Transaction:

A transaction with a related party shall be considered material,

i. If the transaction(s) to be entered into individually or taken together with previous transactions during a financial year,

ii. Exceeds 10% of the annual consolidated turnover of the listed entity

iii. As per the latest Audited Financial Statements.

II. Condition for Related Party Transaction:

a. Prior approval of the audit committee is required and omnibus approval may be given.(sub regulation 2)

b. All material related party transactions shall require approval of the shareholders through a resolution[4]. (sub regulation 4)

c. Related parties shall abstain from voting on such resolutions, whether the entity is a related party to the particular transaction or not - Regulation 23(4). (sub regulation 4)

Abstain from Voting: For the purpose of this regulation, all entities falling under the definition of related parties shall abstain from voting irrespective of whether the entity is a party to the particular transaction or not.

III. Related Party Transactions already entered (Sub Regulation 8):

All existing material related party contracts or arrangements

- Entered into prior to the date of notification of these regulations and

- Which may continue beyond such date

Shall be placed for approval of the shareholders in the first General Meeting subsequent to notification of these regulations.

Non Applicability:

The provisions of sub-regulations (2), (3) and (4) shall not be applicable in the following cases:

(a) Transactions entered into between Two

(b) Transactions entered into between a Holding Company And Its Wholly Owned Subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval.

OMBIOUS APPROVAL BY AUDIT COMMITTEE:[7]

Audit committee MAY grant omnibus approval for related party transactions proposed to be entered into by the listed entity subject to the following conditions, namely-

Conditions for omnibus approval:

a. The audit committee shall lay down the

i. Criteria For Granting the omnibus approval in line with the policy on related party transactions of the listed entity and

ii. Such approval shall be applicable in respect of transactions which are REPETITIVE in nature;

b. The audit committee shall Satisfy Itself regarding the need for such omnibus approval and that such approval is in the interest of the listed entity;

c. the omnibus approval shall specify:

- The name(s) of the related party,

- Nature of transaction,

- Period of transaction,

- Maximum amount of transactions that shall be entered into,

- The indicative base price / current contracted price and

- The formula for variation in the price if any; and

- Such other conditions as the audit committee may deem fit:

Approval of Omnibus transaction without fulfilling the above criteria:

Special Condition: where the need for related party transaction cannot be foreseen and aforesaid details are not available, audit committee may grant omnibus approval for such transactions subject to their value Not Exceeding Rupees One Crore per Transaction.

DUTY OF AUDIT COMMITTEE:

The audit committee shall review, at least on a Quarterly Basis, the details of related party transactions entered into by the listed entity pursuant to Each of the omnibus approvals given.

TERM OF OMNIBUS APPROVAL:

Omnibus approvals shall be valid for a period not exceeding one year and shall require fresh approvals after the expiry of one year.

Compliance requirement: regulation 27(2):

Details of all material transactions with related parties shall be disclosed in compliance report.

The listed entity shall submit a Quarterly Compliance Report on corporate governance in the format as specified by the Board from time to time to the recognized stock exchange(s) within 15 (fifteen days) from close of the quarter.

Disclosure requirement:

i. The listed entity shall disseminate on its website policy on dealing with related party transactions. regulation 46(2)(g)

ii. The annual report of the listed entity shall contain disclosures related party disclosures as specified in Para A of Schedule V. regulation 53 (f)

Role of audit committee:

The audit committee shall mandatorily review statement of significant related party transactions (as defined by the audit committee), submitted by management

CONCLUSITON:

This regulation corresponds to Clause 49VI of the Listing Agreement. The definition of related party in Listing Regulations 2015, continues to define related party as a synthesis of Companies Act, 2013 and Accounting Standard – 18.

Therefore, as per regulation 23(8), all the existing material related party contracts or arrangements entered into prior to the date of notification of these regulations and which may continue beyond such date shall be placed for approval of the shareholders in the first General Meeting subsequent to notification of these regulations. Now the ordinary resolution will suffice the purpose of approval from shareholders instead of special resolution in Listing Agreement.

Still the related parties are abstain from voting on such resolutions whether they are related party to that particular transaction or not.

This point differs with Section 188 of the Companies Act, 2013 whereby the Ministry of Corporate Affairs clarified vide General Circular No. 30/2014 dated 17.07.2014, only the related party in the context of the contract or arrangement were abstained from voting.

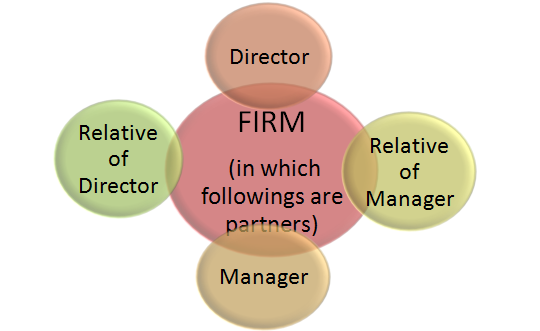

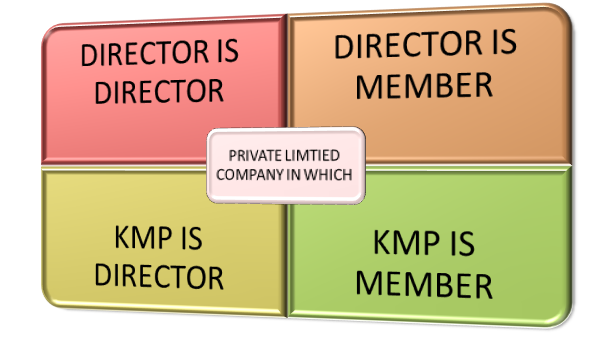

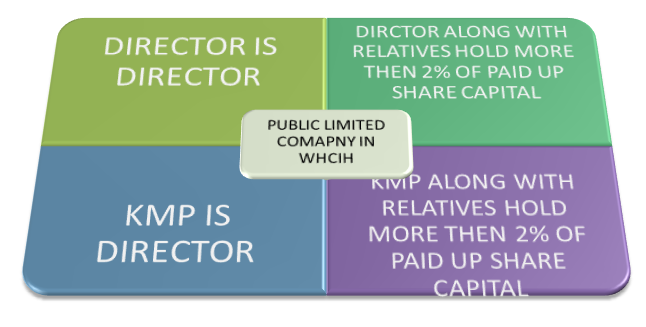

Related Party:

Definition of Related Party as per 2(76) of Companies act, 2013 (DRAWINGS)

[1] Define at the end of the Article

[2] A "transaction" with a related party shall be construed to include a single transaction or a group of transactions in a contract.

[4] Ordinary Resolution.

[5] For the purpose of clause (a), "government company(ies)" means Government company as defined in sub-section (45) of section 2 of the Companies Act, 2013.

[6] Providing For Many Things At Once

[7] As per Section 177(4)(iv) proviso of the Companies Act, 2013 the Audit Committee may make omnibus approval for related party transactions proposed to be entered into by the company subject to such conditions as may be prescribed;

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others