Definition: As stated in section 2(16) “charge” means an interest or lien created on the property or assets of a company or any of its undertakings or both as security and includes a mortgage;

Provisions of Section: As stated in section 78(1) It shall be the duty of every company creating a charge within or outside India, on its property or assets or any of its undertakings, whether tangible or otherwise, and situated in or outside India.

General: Almost all the large and small companies depend upon share capital and borrowed capital for financing their projects. Borrowed capital may consist of funds raised by issuing debentures, which may be secured or unsecured, or by obtaining financial assistance from financial institution or banks.

Security for Lender of Money: The financial institutions/banks do not lend their monies unless they are sure that their funds are safe and they would be repaid as per agreed repayment schedule along with payment of interest. In order to secure their loans they resort to creating right in the assets and properties of the borrowing companies, which is known as a charge on assets. This is done by executing loan agreements, hypothecation agreements, mortgage deeds and other similar documents, which the borrowing company is required to execute in favour of the lending institutions/ banks etc.

Charge” as defined in Transfer of Property Act, 1882

According to Section 100 of the Transfer of Property Act, 1882, where an immovable property of one person is by act of parties or operation of law made security for the payment of money to another and the transaction does not amount to a mortgage, the latter person is said to have a charge on the property, and all the provisions which apply to a simple mortgage shall, so far as may be, apply to such charge.

Terms use under Charge Definition:

- Interest Lien Property

- Assets Undertaking Mortgage

Let’s discuss the meanings of the terms use under the definition of charge:

The meaning of “interest” as per Black’s law dictionary[1]is – ‘legal share in something’.

The meaning of Lien as per the Black’s law dictionary[2]is – ‘a legal right or interest that a creditor has in another’s property lasting usu

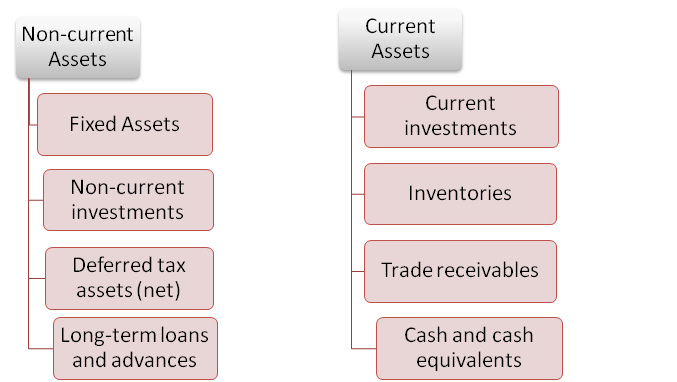

ASSETS

As per Schedule III Assets Include:

ASSETS

A. Fixed assets

|

Tangible assets |

Intangible assets |

|

Classification shall be given as: |

(a) Goodwill; |

|

(a) Land; |

(b) Brands /trademarks; |

|

(b) Buildings; |

(c) Computer software; |

|

(c) Plant and Equipment; |

(d) Mastheads and publishing titles; |

|

(d) Furniture and Fixtures |

(e) Mining rights; |

|

(e) Vehicles |

(f) Copyrights, and patents and other intellectual property rights, services |

|

(f) Office equipment |

(g) Recipes, formulae, models, designs and prototypes; |

|

(g) Others (specify nature). |

(h) Licences and franchise; |

|

(i) Others (specify nature). |

B. Non Current Investment:

- Investment property;

- Investments in Equity Instruments;

- Investments in preference shares;

- Investments in Government or trust securities;

- Investments in debentures or bonds;

- Investments in Mutual Funds;

- Investments in partnership firms;

- Other non-current investments (specify nature).development

Undertaking

Section 180(1)(a) explanation states that:

“undertaking” shall mean an undertaking in which the investment of the company exceeds twenty per cent. of its net worth as per the audited balance sheet of the preceding financial year or an undertaking which generates twenty per cent. of the total income of the company during the previous financial year;

Property

Mortgage:

A mortgage is a legal process whereby a person borrows money from another person and secures the repayment of the borrowed money and also the payment of interest at the agreed rate, by creating a right or charge in favour of the lender on his movable and/or immovable property.

Mortgage as defined in Transfer of Property Act, 1882

According to Section 58 of the Transfer of Property Act, a mortgage is the transfer of an interest in specific immovable property for the purpose of securing the payment of money advanced or to be advanced by way of loan, an existing or future debt, or the performance of an engagement which may give rise to pecuniary liability.

Difference between Charge and Mortgage

In the case of JK (Bombay) Pvt. Ltd. v. New Kaiser-I-Hind Spg. & Wvg.Co. Ltd. AIR 1970 SC 1041 the Supreme Court has distinguished a charge from a mortgage holding that in case of a charge, there is no transfer of property or any interest therein but only the creation of right of payment out of specific immovable property. In contrast, a mortgage effectuates transfer of property or an interest therein

Following types of transactions/agreements are charges and these should be registered with the Registrar of Companies:

a)Mortgage by deposit of title deeds: - According to the Transfer of Property Act, a mortgage on immovable property can be created by depositing the title deeds of the property with the lender as security for the loan. No written instrument is necessary for creating this type of mortgage. It is a common practice to prepare a memorandum of deposit of title deeds listing out the title deeds deposited as a security for the loan. Such mortgage creates a charge on the property mortgaged. Hence, it must be registered as a charge.

b) Charge created by a Company merged with another Company- When a Company is amalgamated with another Company pursuant to the High Court’s order under section 394 of the Act, the transferee-Company should file form CHG-1 with the Registrar, in respect of property of the transferor-Company, acquired by it, subject to charge.

|

Principle rule of Creation of Charge is that “Charge will be creating only on the Assets of the Company�, Assets as defined in Schedule III of the CA-2013. |

As per definition of the Charge “A charge shall be created on the Assets/Property/Undertaking of the Company”. Therefore, following questions arise from this definition:

FAQ’S

I. Whether charge will create on hypothecation of vehicle.

We keep on receiving queries time and again as to whether Hypothecation of Motor Vehicle can be termed as “charge” and whether this charge is required to be registered? Section 77(1) of the Act has simply changed the list that was provided in the Companies Act, 1956 and requires registration of each and every charge created on the asses of the Company whether tangible or otherwise, and situated in or outside India.

There is specific option given in e-form CHG-1 charge on “Vehicle(hypothecation)”. It is clear that there is need to crate charge on hypothecation of vehicle under Companies Act, 2013.

Definition of Hypothecation:

Section 3 (n) of the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act) defines 'hypothecation as:

"Hypothecation" means a charge in or upon any movable property, existing or future, created by a borrower in favour of a secured creditor without delivery of possession of the movable property to such creditor, as a security for financial assistance and includes floating charge and crystallization of such charge into fixed charge on movable property.

II. Whether charge will create on Pledge.

Earlier there was list of transaction on which charge was required to create. With the enactment of the Companies Act, 2013, tire list of charges requiring registration done away with. Thus, in the absence of a specific list of charges to be registered, and the wide definition of the word “charge”, ‘pledges’ and ‘liens’ were also required to be registered.

The companies creating pledge over shares are compulsorily required to register the charge, which was not the case with its predecessorThis question I have discussed in details in my separate article.

Definition of Pledge:

Section 172 of the Indian Contracts Act, 1872 defines a pledge as:

"The bailment of goods as security for payment of a debt or performance of a promise is called "pledge"."

In simple terms a pledge is a security created on movable goods of the borrower or pledgor for the payment of a debt wherein the lender or pledgee takes actual possession of the goods until the entire debt amount is repaid by the borrower. The pledgee may retain the goods pledged, not only for payment of the debt or the performance of the promise, but for the interests of the debt, and all necessary expenses incurred by him in respect to the possession or for the preservation of the goods pledged.

III. Whether there is need to create charge on the personnel guarantee of the Promoters.

As per principle rule, Personnel guarantee of the Promoters are not assets of the Company. Therefore, there is no need to create charge on the personnel guarantee of the promoters.

IV.There are two Companies ABC Pvt Ltd and PQR Pvt Ltd. ABC Pvt Ltd taking loan from the Bank and PQR giving guarantee on its property.

Whether Charge will be created in ABC Pvt Ltd?

Whether charge will be created in PQR Pvt Ltd?

- As per principle rule, In the above situation PQR is giving its assets as security to bank for loan to ABC, therefore assets of the PQR is involved charge will be create in the PQR Pvt Ltd.

- Here assets of the ABC are not involved in the security, therefore no need to create charge in ABC Pvt Ltd.

V. Whether Guarantee given by Company to other Company amount to creation of Charge.

Sometimes companies give counter-guarantee to banks for the guarantee given by the banks to the Government or other authorities. Such a guarantee does not create any encumbrance on the company’s properties. So, it need not be registered- S.T. Patil V. Registrar of Companies 10 CC

VI. Whether charge will be create on FDR of the Company.

- Deposit of a fixed deposit receipt with the Bank by way of security for a loan amount to pledge of movable property. There is required to create charge on pledge under Companies Act, 2013. Conclusion, So it need to be registered.

Under CA-1956 there was not required to create charge on pledge at that time in a case of Sree Meenakshi Mills Ltd. V ROC (1966) decisions was there is no need to register charge on fixed deposit.

VII. Whether charge can be create on future assets of the Company.

- As per principle rule, Future assets are not part of the assets side of the balance sheet of the Company. Company can’t create security on the same. Therefore, no need of creation of charge on the future assets of the Company.

VIII. What is the time period to file CHG-1 with ROC in case of creation of security out of India?

In the case of a charge created out of India, and comprising solely property situate outside India, thirty days after the date on which the instrument creating or evidencing the charge or a copy thereof could, in due course of post and if dispatched with due diligence, have been received in India, shall be substituted for 4hirty days after the date of the creation of the charge, at the time within which the particulars and instrument or copy are to be filed with the Registrar.

IX. Whether enhancement of a loan amounts to modification

Provision: As per section 79 Company required to file form for modification of charge for 4 (four) purposes. Any modification in the terms or conditions or the extent or operation of any charge registered under that section.

Example: In the case of companies it is a normal practice that they obtain working capital facilities from banks. There working capital facilities are usually secured by a charge on the current assets of the company. Whenever the working capital facilities are increased a company is required to give additional security which means the existing charge has to be enhanced to cover the enhanced limits, by filing CHG-1 with ROC.

X. Whether Charge will be create on hire purchase agreement?

A hire purchase agreement place the financier in the position of a secured creditor. So a hire purchase agreement must be registered as a charge- Official Liquidator, Manasuba & Co. (P.) Ltd. V. Commissioner of Police {1968}

XI. From which date charge consider as register.

It was held in the case of SBI v. Haryana Rubber Industries (P.) Ltd. [1986] 60 Comp Cas 472 (Punj. & Har.) that the charge stands registered from the date of filing of particulars even if the ROC delays making entries in his books.

Moreover, it was held in the case of Official Liquidator v. Union Bank of India that non-compliance does not mean that the transaction is void or debt is not recoverable. Only consequence is that security becomes void as against liquidator and creditors

XII. In case Company fails to register the charge, when the charge holder got right to file the form with ROC?

Language of Provision:

i.Section 78 Where a company fails to register the charge within the period specified in section 77, without prejudice to its liability in respect of any offence under this Chapter, the person in whose favour the charge is created may apply to the Registrar for registration of the charge

ii. Section 77 It shall be the duty of every company creating a charge in such form, on payment of such fees and in such manner as may be prescribed, with the Registrar within thirty days of its creation

Opinion:

As per combined reading of Section 77(1) and section 78(1) it is clear that Charge holder can apply for creation of charge to registrar (when company fails to register chare within period mention in section 77) after expiry of 30 days of its creation.

Therefore, charge holder get right of create of charge w.e.f 31st day of creation of charge.

XIII. Whether register of charge can be maintain at any place other then registered office of the Company.

As stated in rule 10(1) registers shall be kept at the registered office of the Company. Company can’t maintain the register of Charge at any other place.

XIV. Who can authenticate the entry in the Register of Charge?

Entries in the register shall be authenticated by a director or the secretary of the Company or any other person authorized by the Board for the purpose

XV. Who can inspect the register of Charge of the Company?

- Any member or creditor of the company without fees;

- Any other person on payment of fee.

XVI. Whether provision of charge will be applicable on One Person Company?

The provisions of this chapter shall apply mutatis mutandis to One Person Company.

[1 ]9th Edition, page no.885

[2] 9th Edition, page no. 1006

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Corporate Law